Introduction: Why Homeowners Insurance Matters in Indiana

Buying a home is one of the biggest financial decisions most people will ever make. In Indiana, where homes are often affordable compared to coastal states, many homeowners underestimate how important proper insurance coverage really is.

Homeowners insurance is not just a box to check for your mortgage lender. It is a financial shield that protects your home, your belongings, and your long-term stability when unexpected events happen.

From Midwest storms and tornado risks to fire, theft, and liability claims, Indiana homeowners face real exposures. The right insurance policy doesn’t eliminate risk—but it makes risk manageable.

This guide explains how to buy homeowners insurance in Indiana, what coverage really means, how to compare policies, and how to avoid common mistakes that cost homeowners money when it matters most.

What Is Homeowners Insurance?

Homeowners insurance is a policy that protects you financially if your home or belongings are damaged or if someone is injured on your property.

A standard policy typically covers:

- The structure of your home

- Personal belongings

- Liability protection

- Additional living expenses if your home becomes unlivable

In Indiana, homeowners insurance is not required by state law—but almost every mortgage lender requires it.

Why Indiana Homeowners Need Insurance

Indiana homeowners face a unique mix of risks.

Common risks include:

- Severe thunderstorms

- Tornadoes

- Hail damage

- Winter-related damage (frozen pipes, ice)

- Fire

- Theft and vandalism

Even a single event can result in tens of thousands of dollars in damage. Insurance turns a financial disaster into a manageable claim.

Who Needs Homeowners Insurance in Indiana?

If you:

- Own a single-family home

- Own a townhouse or condo (with appropriate policy type)

- Are purchasing a home with a mortgage

…you need homeowners insurance.

Even homeowners without a mortgage should strongly consider coverage. Paying off your house does not remove risk—it removes the bank’s protection, not yours.

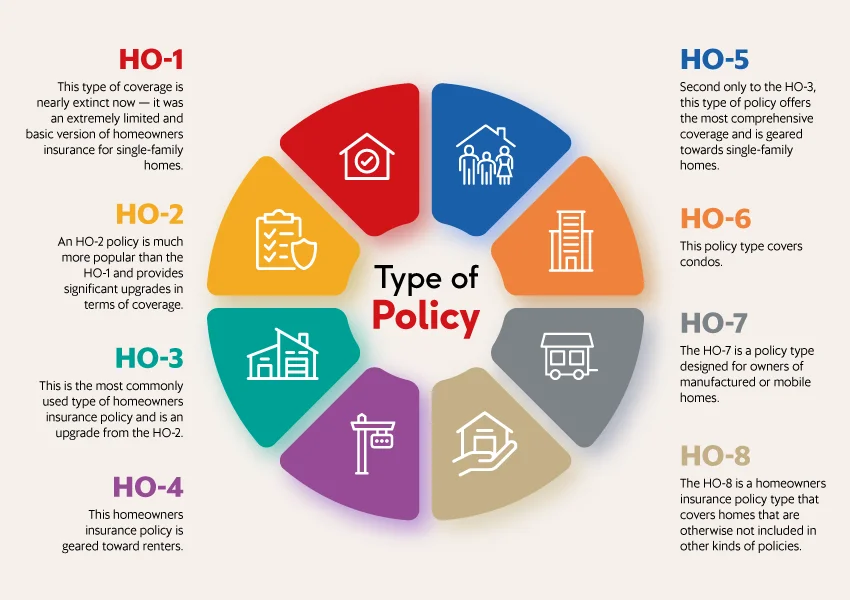

Types of Homeowners Insurance Policies

Understanding policy types helps you choose correctly.

HO-3 (Most Common in Indiana)

- Covers your home for all risks except exclusions

- Covers belongings for named perils

This is the most popular and flexible option.

HO-1 and HO-2

- Limited coverage

- Less common today

HO-5

- Broader coverage for both home and belongings

- Higher premiums, stronger protection

HO-6 (Condo Insurance)

- For condo owners

- Covers interior and personal property

HO-4 (Renters Insurance)

- For renters, not homeowners

Most Indiana homeowners choose HO-3 policies.

What Does a Standard Indiana Homeowners Policy Cover?

1. Dwelling Coverage

Protects the physical structure of your home.

This includes:

- Walls

- Roof

- Foundation

- Built-in appliances

Coverage should reflect rebuild cost, not market value.

2. Other Structures Coverage

Covers structures not attached to your house:

- Garages

- Sheds

- Fences

Typically 10% of dwelling coverage.

3. Personal Property Coverage

Protects your belongings:

- Furniture

- Electronics

- Clothing

- Appliances

Usually 50–70% of dwelling coverage.

4. Liability Protection

Covers you if someone is injured on your property or you damage someone else’s property.

This is one of the most underrated but valuable parts of the policy.

5. Loss of Use (Additional Living Expenses)

Pays for:

- Temporary housing

- Meals

- Extra costs

…if your home becomes unlivable due to a covered loss.

What Is NOT Covered by Standard Policies?

This is where many homeowners get surprised.

Standard policies usually do NOT cover:

- Flood damage

- Earthquakes

- Sewer backups (unless added)

- Wear and tear

Indiana homeowners should seriously consider flood insurance, especially in areas near rivers or with poor drainage.

Flood Insurance in Indiana: An Important Add-On

Flood damage is excluded from standard policies—even if caused by heavy rain.

Flood insurance:

- Is purchased separately

- Is often required in high-risk zones

- Can be affordable outside flood plains

Indiana has many flood-prone areas, especially near rivers and low-lying land.

How Much Does Homeowners Insurance Cost in Indiana?

Indiana is generally considered a moderate-cost state for homeowners insurance.

Premiums depend on:

- Home value

- Location

- Construction type

- Claims history

- Coverage limits

- Deductible amount

Compared to national averages, Indiana homeowners often pay less than high-risk states, but costs still vary widely.

Factors That Affect Your Premium

Location

Urban vs rural areas

Proximity to fire departments

Crime rates

Home Characteristics

Age of home

Roof type

Square footage

Building materials

Personal Factors

Claims history

Credit-based insurance score

Deductible selection

Choosing the Right Coverage Amount

Replacement Cost vs Market Value

Insurance should cover rebuilding your home, not resale price.

Land value does not need to be insured.

Underinsuring saves money short term—but costs massively after a loss.

Replacement Cost vs Actual Cash Value

- Replacement Cost: Pays to replace items new

- Actual Cash Value: Deducts depreciation

Replacement cost coverage is strongly recommended.

Deductibles: Choosing Wisely

A deductible is what you pay out of pocket before insurance pays.

Higher deductible:

- Lower premium

- Higher out-of-pocket risk

Lower deductible:

- Higher premium

- Less financial shock during claims

Indiana homeowners often choose deductibles between $1,000–$2,500.

Shopping for Homeowners Insurance in Indiana

Step 1: Gather Home Information

- Square footage

- Year built

- Roof age

- Safety features

Step 2: Compare Multiple Quotes

Never buy from the first quote alone.

Compare:

- Coverage limits

- Deductibles

- Exclusions

- Company reputation

Local vs National Insurance Companies

National Insurers

- Strong financial backing

- Advanced online tools

- Broad coverage options

Local or Regional Insurers

- Familiar with Indiana-specific risks

- Personalized service

Both can be good—focus on coverage quality.

Bundling Insurance Policies

Bundling homeowners with:

- Auto insurance

- Umbrella policies

…often results in discounts of 10–25%.

Bundling simplifies management and reduces costs.

Discounts You May Qualify For

Indiana insurers may offer discounts for:

- Security systems

- Smoke detectors

- New roofs

- Claims-free history

- Multi-policy bundles

Always ask—discounts are not automatic.

Reading the Policy: What to Pay Attention To

Key sections to review:

- Coverage limits

- Exclusions

- Endorsements

- Claims process

Understanding before you need it is critical.

Common Mistakes Indiana Homeowners Make

Avoid these:

- Underinsuring the home

- Ignoring flood risk

- Choosing the cheapest policy

- Not updating coverage after renovations

Cheap insurance is expensive after a loss.

Filing a Homeowners Insurance Claim

When a loss occurs:

- Ensure safety first

- Document damage

- Contact your insurer promptly

- Keep receipts

Clear communication speeds resolution.

How Claims Affect Future Premiums

Filing claims may:

- Increase premiums

- Impact renewal eligibility

Use insurance for major losses—not minor maintenance.

The CEO Mindset: Treat Insurance as Risk Management

Smart homeowners think like business owners.

Insurance is not an expense—it’s risk transfer.

Ask:

- What risks can I afford?

- What risks should I insure?

Strategic coverage protects long-term wealth.

Reviewing and Updating Your Policy Annually

Life changes—so should coverage.

Review when:

- Home value changes

- Renovations are completed

- Property is acquired

- Risks change

Annual reviews prevent costly gaps.

First-Time Homebuyers in Indiana

If this is your first home:

- Ask questions

- Don’t rush decisions

- Focus on protection, not price

First impressions from insurers can shape years of coverage.

Homeowners Insurance and Mortgages

Lenders require:

- Proof of insurance

- Coverage effective before closing

Failing to maintain coverage can trigger forced insurance—usually expensive and limited.

Long-Term Benefits of Proper Coverage

Well-insured homeowners enjoy:

- Financial stability

- Faster recovery after loss

- Peace of mind

- Protection of equity

Insurance doesn’t prevent damage—it prevents devastation.

Final Thoughts: Buy Coverage, Not Just a Policy

Buying homeowners insurance in Indiana is not about finding the cheapest quote.

It’s about:

- Understanding your risks

- Choosing appropriate protection

- Working with reliable insurers

Your home is more than a building—it’s security, comfort, and long-term value.

Protect it wisely.

Word Count:

304

Summary:

Did you know that according to the Indiana Department of Insurance (IDI), the insurance industry is one of Indiana’s largest employers. That being said, that means there are many insurance options for homeowners in Indiana. Because the insurance industry is so large, there must be tough regulation to ensure the protection of the consumer.

Here are some facts Indiana homeowners should be aware of when securing homeowners insurance:

If your homeowners policy is being canc…

Keywords:

Article Body:

Did you know that according to the Indiana Department of Insurance (IDI), the insurance industry is one of Indiana’s largest employers. That being said, that means there are many insurance options for homeowners in Indiana. Because the insurance industry is so large, there must be tough regulation to ensure the protection of the consumer.

Here are some facts Indiana homeowners should be aware of when securing homeowners insurance:

If your homeowners policy is being cancelled for non payment of premium, the notice of cancellation must be in writing and sent to you at least 10 days before policy cancellation.

If your insurance company does not want to renew your policy, IDI requires the notice be sent to you at least 20 days before policy expiration. As a consumer, negotiate with your insurance company to extend the 20 days to 30 or 60 day notice. If your policy is being cancelled for a reason other than non payment, you’ll need the extra time to shop around for replacement coverage.

If your policy does not cover flood damage, it must be stated prominently on the policy jacket or, you must be given written notice that flood coverage may be available through the National Flood Insurance Program.

In certain Indiana counties in southwestern Indiana along the Illinois Coal Basin, the insurance company must inform you of the availability of mine subsidence coverage (coverage for homes built over mines that may collapse or slowly settle) when they issue the policy.

IDI also regulates how much an insurance company can charge you for an inadvertent bad check. Their charge may not exceed $20 (this is in addition to the charge issued by the banking institution).

Please see our list of references below to find the lowest rate insurance quotes on the web. Along with low rate quotes this is a good source of insurance information.

Tinggalkan Balasan