Introduction: Life Insurance Is Not About Death—It’s About Responsibility

Life insurance is one of the most misunderstood financial tools.

Many people delay buying it because it feels uncomfortable, complicated, or unnecessary—until it suddenly becomes urgent. The reality is simple: life insurance is not about planning for death, it’s about protecting life while you’re alive.

It protects your family, your business, your future plans, and the people who depend on you financially. Buying life insurance without a plan often leads to overpaying, under-coverage, or choosing the wrong product altogether.

That’s why you need a clear shopping checklist.

This article walks you through a practical, step-by-step checklist to help you buy life insurance confidently, intelligently, and without regret.

Why You Need a Checklist Before Buying Life Insurance

Life insurance shopping is emotional—and emotional decisions are often expensive.

A checklist helps you:

- Avoid pressure-based sales

- Buy the right amount of coverage

- Choose the correct policy type

- Control costs

- Protect long-term goals

Think of this like buying a business asset, not a consumer product.

Checklist Item #1: Clarify Why You Need Life Insurance

Purpose Comes Before Policy

Before looking at numbers or quotes, answer one question:

Who would be financially impacted if you weren’t here tomorrow?

Common reasons people buy life insurance include:

- Income replacement for family

- Paying off mortgage or debts

- Funding children’s education

- Business continuity

- Covering final expenses

Life insurance is about replacing economic value, not emotional value.

Checklist Item #2: Identify Who Depends on You Financially

Make a clear list:

- Spouse or partner

- Children

- Aging parents

- Business partners

If no one relies on your income, you may need less—or no—life insurance.

If multiple people rely on you, coverage becomes critical.

Checklist Item #3: Decide How Much Coverage You Actually Need

Avoid Guessing—Use Logic

One of the biggest mistakes is choosing coverage based on emotion instead of math.

Start with:

- Annual income

- Number of years income needs to be replaced

- Outstanding debts

- Major future expenses

A common guideline is 10–15× annual income, but your real needs may be higher or lower.

Checklist Item #4: Account for Existing Assets and Coverage

Before buying new coverage, review what you already have:

- Employer-provided life insurance

- Savings and investments

- Retirement accounts

Employer coverage is often:

- Temporary

- Limited

- Not portable

Do not rely on it alone.

Checklist Item #5: Choose the Right Type of Life Insurance

Term vs Permanent Insurance

This decision impacts cost more than anything else.

Term Life Insurance

- Coverage for a fixed period (10–30 years)

- Lower cost

- Pure protection

Best for:

- Income replacement

- Young families

- Mortgage protection

Permanent Life Insurance (Whole / Universal)

- Lifetime coverage

- Higher premiums

- Includes cash value

Best for:

- Estate planning

- Business needs

- Long-term wealth strategies

For most people, term life is the smartest starting point.

Checklist Item #6: Decide How Long You Need Coverage

Match coverage length to responsibility length.

Examples:

- Until children are financially independent

- Until mortgage is paid off

- Until retirement savings are sufficient

Buying coverage longer than necessary increases cost without added benefit.

Checklist Item #7: Set a Realistic Budget

Life insurance should fit your cash flow comfortably.

A good policy:

- Protects without stress

- Does not require lifestyle sacrifice

Term insurance is designed to be affordable—even substantial coverage often costs less than daily coffee habits.

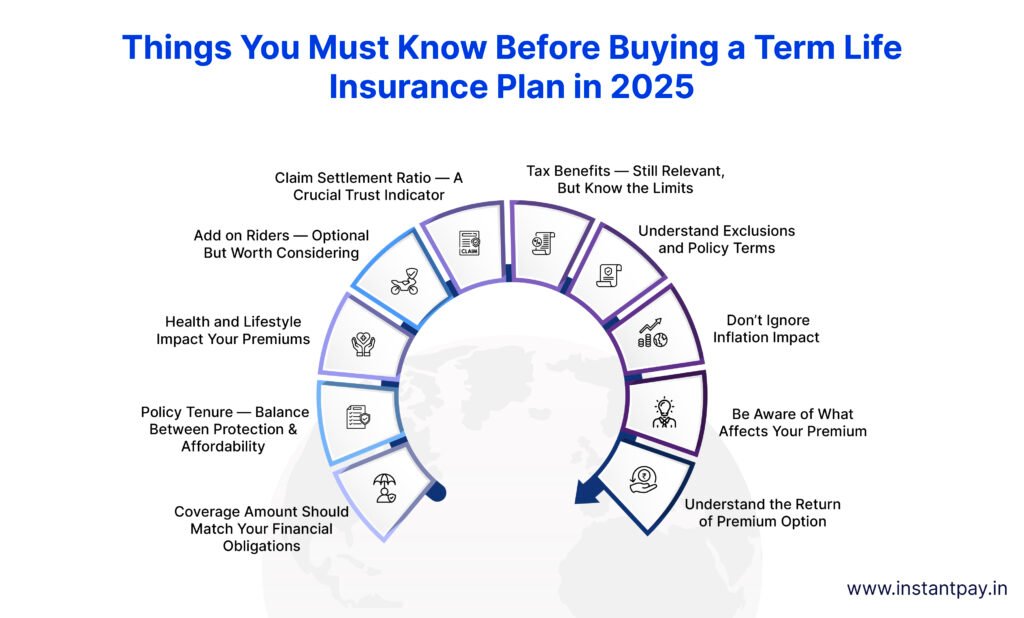

Checklist Item #8: Understand What Affects Your Premium

Life insurance pricing depends on:

- Age

- Health

- Lifestyle (smoking, risky hobbies)

- Coverage amount

- Policy type

The younger and healthier you are, the cheaper coverage is.

Waiting almost always costs more.

Checklist Item #9: Prepare for the Medical Underwriting Process

Many policies require:

- Health questionnaires

- Medical exams

- Blood or urine tests

Honesty matters.

Misrepresentation can void coverage when your family needs it most.

Checklist Item #10: Compare Quotes—Not Just Prices

Never buy from the first quote alone.

Compare:

- Premiums

- Policy terms

- Riders

- Company financial strength

The cheapest policy is not always the best.

Checklist Item #11: Evaluate the Insurance Company

Life insurance is a long-term promise.

Look for:

- Financial strength ratings

- Claims reputation

- Longevity in the market

Your policy is only as strong as the company behind it.

Checklist Item #12: Understand Policy Riders (Optional Add-Ons)

Common riders include:

- Waiver of premium

- Accelerated death benefit

- Child riders

Riders add flexibility—but also cost.

Only add what serves your purpose.

Checklist Item #13: Choose Beneficiaries Carefully

Your beneficiary selection determines who receives the payout.

Tips:

- Name primary and contingent beneficiaries

- Avoid vague designations

- Review after major life events

Incorrect beneficiary setup can cause delays or legal issues.

Checklist Item #14: Consider Inflation and Future Needs

What feels like enough coverage today may not be enough in 15 years.

Options:

- Buy slightly more upfront

- Choose longer-term coverage

- Reevaluate periodically

Planning ahead reduces future stress.

Checklist Item #15: Avoid Mixing Insurance With Investments (Unless You Fully Understand It)

Some policies combine life insurance with investment features.

These can work—but only when:

- You understand fees

- You understand returns

- The purpose justifies the cost

For most people, simple protection + separate investing works better.

Checklist Item #16: Work With a Professional—But Stay in Control

An agent can help—but remember:

- You are the decision maker

- Ask questions

- Take time

Never feel rushed into signing.

Pressure is a red flag.

Checklist Item #17: Read the Policy Before You Sign

Key sections to review:

- Coverage amount

- Term length

- Exclusions

- Renewal terms

If you don’t understand it, ask.

Checklist Item #18: Store Your Policy Information Securely

Make sure someone you trust knows:

- Where the policy is

- Who the beneficiaries are

- How to file a claim

An unknown policy is a useless policy.

Checklist Item #19: Review Coverage After Life Changes

Review your policy when:

- You get married

- Have children

- Buy a home

- Change careers

Life insurance should evolve with life.

Checklist Item #20: Revisit Your Plan Every Few Years

Even if nothing changes, review periodically:

- Coverage still appropriate?

- Better rates available?

- Beneficiaries correct?

Insurance should never be “set and forget.”

Common Life Insurance Buying Mistakes

Avoid these:

- Waiting too long

- Buying too little

- Buying permanent insurance unnecessarily

- Naming minor children directly as beneficiaries

Simple mistakes can have long-term consequences.

The CEO Mindset: Life Insurance as Risk Management

Smart leaders insure against catastrophic loss.

Life insurance is:

- A balance-sheet stabilizer

- A family protection tool

- A business continuity asset

It’s not emotional—it’s strategic.

Life Insurance Is an Act of Leadership

Buying life insurance is not about fear.

It’s about:

- Responsibility

- Preparation

- Care for others

It’s one of the most practical financial decisions you can make.

Final Thoughts: Use the Checklist—Buy With Confidence

Life insurance doesn’t have to be confusing or stressful.

With the right checklist, you:

- Buy the right coverage

- Avoid overpaying

- Protect what matters most

Don’t rush.

Don’t guess.

Don’t delay.

Buy life insurance the same way you’d run a business decision—with clarity, intention, and confidence.

Word Count:

1194

Summary:

When shopping for term life insurance, you want to find the right amount of insurance coverage at a reasonable price with a company you can trust. But for many people, getting started is the hardest part. That’s where the following Life Insurance Checklist can help.

Keywords:

life insurance quote comparison

Article Body:

When shopping for term life insurance, you want to find the right amount of insurance coverage at a reasonable price with a company you can trust. But for many people, getting started is the hardest part. That’s where the following Life Insurance Checklist can help.

- What you would like your policy to achieve?

Ask yourself what it is you want your life insurance to do. For example, do you want to have insurance coverage that will:

� Pay funeral arrangements?

� Pay the outstanding balance owing on a mortgage and other debts?

� Offset the loss of your income? And if so, for how long?

� Contribute to the future education of your children?

� A combination of all or part of the above?

Knowing what you would like to accomplish with your life insurance policy and approximately how much you need to achieve these goals will help you determine how much life insurance you should consider purchasing. Online life insurance calculators are available to help you put a dollar value on the amount of coverage you need.

- Who would you like to insure under the life insurance policy?

Most insurance companies offer a variety of life insurance products to suit your lifestyle and family needs. You can get an insurance policy on your own life, or you can get one policy for both you and your spouse (called a joint life insurance policy). The most common joint life policy provides coverage when the first partner dies, leaving the life insurance benefit to the surviving spouse. - How long will you need life insurance?

Consulting a psychic isn�t necessary, although it does require that you estimate the timing of your life insurance needs. For example:

� When will your mortgage be paid off? The amortization period of your mortgage will often determine how long your term life insurance policy should be.

� When will your children be finished school? One day they’ll finish their education and having enough life insurance coverage to pay their educational expenses won’t be necessary.

� When are you planning to retire? You will have less income to replace at that time.

Knowing how long you�ll need life insurance coverage before you begin shopping will ensure you’re comfortable with the life insurance product you end up purchasing. Online tools are available to help you figure out which term for your life insurance policy is most recommended for people with similar lifestyles.

So now that you’ve got the how much, who and how long questions answered, you�re ready to shop.

- Compare life insurance quotes from multiple companies:

It pays to shop around because life insurance rates can vary considerably depending on the product you choose, your age, and the amount of coverage you request. This is the easy part, because with the Internet you can compare life insurance quotes easily, online, anytime. - Which life insurance rate has been quoted � standard or preferred?

There are two basic life insurance rate groups you should know about when shopping for life insurance coverage: standard rates and preferred. Standard life insurance rates are the rates the majority of Canadians qualify for, while about one third of the population is eligible for preferred rates.

Preferred life insurance rates are typically offered to very healthy people and means you may pay a smaller premium than most. Usually preferred rates are offered only once the results of the medical information and tests are known. It will depend on your blood pressure, cholesterol levels, height, weight, and family health history. But preferred rates are worth it. They could save you up to 30-35% off your quoted premium.

When comparing prices, make sure you’re comparing ‘standard to standard’ or ‘preferred to preferred’ life insurance rates. If you’re not sure, ask the broker. It would be disappointing to find out you were quoted preferred rates at the beginning, only to find out you don’t qualify for them later.

- Review the life insurance broker’s availability:

How easily can you get a hold of the broker? What are their hours of operation? Whether it is through their website or telephone, the life insurance broker should be easily accessible to you should you ever have questions or need to speak to them about a change in your life insurance needs. Look for toll-free numbers and extended hours of service as guides. - Review the medical information required to obtain the policy:

Typically the more medical information you provide, the better the price. For a policy that asks few or no medical questions, you can bet the premium is higher for the same coverage then a plan asking for more information. Depending on the company, your age, and the amount of coverage you want, you could be asked to provide blood and urine samples. To obtain the samples, a nurse will visit at not cost to you. - Consider a life insurer’s financial stability and strength:

A company’s financial stability is something to consider if you are planning on making a long-term purchase like life insurance. There are organizations out there, like A.M. Best, that evaluate insurers and provide a rating on their stability and strength. - Ask about renewal options and requirements:

Once the initial premium is set, it is usually guaranteed for the length of the policy (often 10 or 20 years). But what happens when the policy expires? Most policies are renewable until you are 70 or 75 so don’t forget to ask your broker if you will have to take a medical to renew your policy. While your premiums will be higher on renewal, find out if they will also be guaranteed to remain level for the second term of the policy. - Confirm the policy can be cancelled without penalty:

Most term life insurance policies can be cancelled at any time without penalty. Make sure to check with your broker to see if the life insurance company has any unusual cancellation policies. - Consider the conversion options and restrictions for the policy:

As your life changes so do your life insurance needs and you may want the option to convert your coverage some day.

To convert a term life insurance policy means to transfer all, or part of, the death benefit of the policy into a permanent life policy without a medical. For example, say you originally bought a term policy to protect a mortgage and child. Once the mortgage is paid and the child grown, you might find it desirable to convert the policy into one that will give you a new level premium for the rest of your life, and a death benefit that is guaranteed not to expire as you age.

When you purchase your life insurance policy, find out if there are any limitations on your age at the time of conversion. In most cases, you have the option of converting up until you are 60 or 65. As well, ensure you are given several options of the type of policies you can move into, the more the better.

Final tip � choose a life insurance broker you trust:

While it doesn’t necessarily impact the type of policy you choose to purchase, a rapport with your broker is critical in feeling comfortable with the life insurance policy you buy and the information you’ve received.

Tinggalkan Balasan